The price of oil has fallen from its peak near the beginning of the Russian invasion of Ukraine, but people who work in the energy industry expect volatility to continue. Monday afternoon, the price of West Texas Intermediate crude was $103.75, up from $99.27 Friday but down from a peak of $123.70 March 8.

Bob McNally, president of the consulting firm, Rapidan Energy Group, an energy, policy and geopolitical consulting firm in Washington D.C., says demand for oil is less elastic than demand for other products.

"What would happen if Total Wine announced all cabernets are 75% off next week? I don't know about you, but I'd get a truck and go to Total Wine. Demand would go up," he says. "But what would happen if gasoline prices, and this would be nice, fell from four dollars to $1.50 next week? Would you get in the car and say, 'Honey, I'll be back. I'm just going to go to Austin and back because this is just awesome'? You wouldn't. Conversely, if oil prices go way up, are you going to say, 'I'm not going to work. I'm not paying the price'?"

McNally spoke at TCU's Global Energy Symposium. He says that "inelastic" relationship between supply and demand leads to bigger price swings to balance the market.

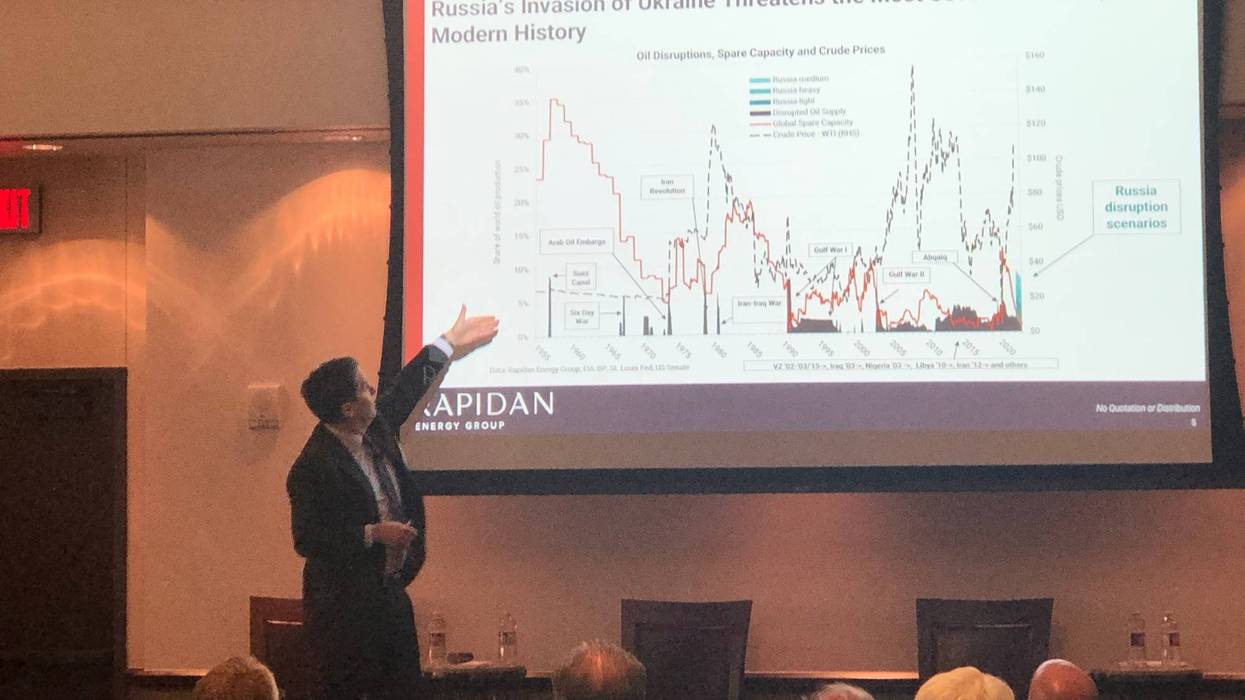

He says Russia has been producing about seven million barrels of oil a day, but OPEC countries have just 2.5 million barrels in spare capacity.

"We're low on spare, and we're high on disruption," he says. "That is a disaster for the economy. When you have a war, that comes in handy. It's like an emergency supply of the life-blood of modern civilization."

McNally says the greatest disruption to oil production was the 1956 Suez Crisis. During the Suez Crisis, though, he says the U.S. and other countries were holding about a third of oil production capacity to keep prices stable.

"It's really hard for the world to manage this kind of volatility," he says, joking that before OPEC was created, the Texas Railroad Commission had to practice communism in order to ensure stable prices. "That's why it impelled places like Texas to resort to communism. It's really, really difficult."

Without the same spare production available now, McNally says price swings will continue with uncertainty in Russia and Ukraine. He says the discussion over the Keystone XL Pipeline became "hyper political," saying the pipeline should be built. McNally also says shale producers are struggling to find labor and materials.

"They are shell-shocked," he says. "Everyone's saying the shale companies must be feeling like they've got swagger now. President Biden's calling them up saying, 'please, please, please, you've got to put a rig out there.' That's not what I'm hearing. The shale companies, just like OPEC+, are still traumatized by May of 2020 and, for that matter, 2015."

He also says another spike in oil prices could drive more interest in a shift to electric cars, but McNally describes energy transitions as "rare and hard." He says government demands for improved fuel efficiency or electric cars may not be as successful as incentives for new products.

"For five millennia, if a human being wanted to go faster over land than he or she could walk, your option was a horse," he says. "Yet now, we're going to the moon, we're driving cars. Was that because of a 'peak horse' policy or government intervention? No, that was because, thank God, capitalistic economies in the UK and United States incentivized people to think of new technologies."

LISTEN on the Audacy App

Sign Up and Follow NewsRadio 1080 KRLD